Anticipating Rate Cuts: Implications for Asset Pricing and Risk

After a disappointing year (for many) on the Australian interest rate front in 2024, expectations are heightened for multiple cuts to domestic interest rates in 2025, particularly given recent data. Such cuts will, in turn, have ramifications on asset values, pricing, and risk – but to what end? In this inaugural Monthly Insights, a piece that Harbour Credit Partners (HCP) intends to publish regularly to succinctly address contemporaneous matters and to keep our investors abreast of the firm’s thinking, we examine the interplay between rates and asset values in the residential property space, and whether assumed norms have played out historically. We then summarise how HCP approaches underwriting given these dynamics.

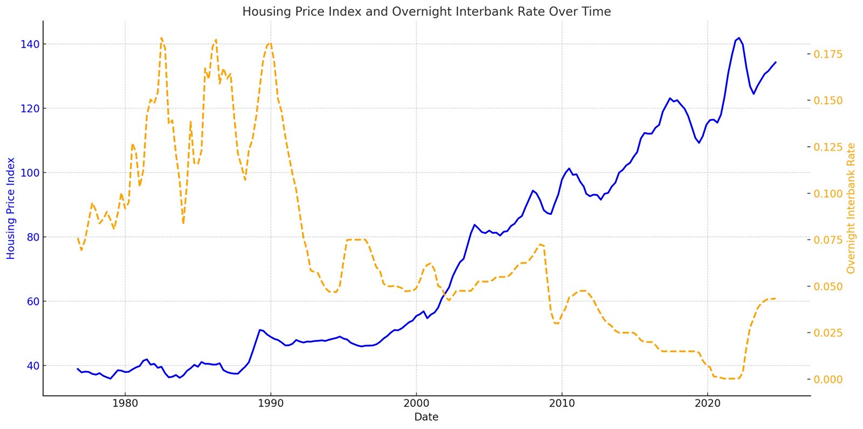

What Does the Data Say About Rates and Asset Values?

Data sourced from: Australian Bureau of Statistics (2024)

Given our high exposure, we will focus our analysis on residential property. While the relationship between interest rate changes and residential property values is often discussed, historical data paints a more nuanced picture. Analysis spanning 50 years, back to the 1970s, reveals a high degree of negative correlation (-0.79) between interest rate changes and residential real estate price movements over that entire period. Such a result verges on common knowledge: low(er) rates cause a rally in residential property prices.

This ‘helicopter view’ over a half century can distort the reality over shorter periods. Zooming in, we observe several sub-periods within the 1970s, 1990s, 2000s and, indeed, the last several years where the relationship between interest rates and house prices are either positively correlated (as opposed to inversely correlated) or uncorrelated (a change in rates had a negligible effect on housing prices). This suggests that other factors – such as economic growth, supply-demand imbalances, fiscal policies, and geopolitical trends – also play a significant role in shaping residential property asset values. Predicting the direction of rates and their precise impact on valuations is, therefore, fraught with uncertainty in the absence of perfect foresight into these other factors as well.

Should Market Expectations Inform Underwriting?

Market expectations are an important consideration but not a definitive guide. While they can provide context, overreliance on speculative forecasts risks introducing bias into decision-making.

At HCP, market sentiment is just one input among many. Our underwriting process prioritises empirical evidence, historical analysis, and scenario testing. Regular updates to our models ensure that we adapt to changing conditions without compromising discipline. When sentiment strongly influences a transaction, we apply higher risk premiums to better reflect the inherent risks.

How Does Harbour Credit Partners Think About Risk and Pricing?

HCP’s pricing and risk framework revolves around three key principles:

1. Scenario Analysis: We consider multiple economic scenarios, including those where rates fall, rise, or remain stable, to understand potential risks and opportunities.

2. Stress Testing: Transactions are rigorously tested against downside scenarios, such as economic shocks or valuation corrections, ensuring resilience in diverse conditions.

3. Behavioural Insights: Markets often overreact to expected rate movements, creating speculative pricing bubbles. HCP remains focused on fundamentals to avoid being swept up in short-term sentiment.

This disciplined approach helps us align pricing and risk management with long-term portfolio stability.

HCP will also adopt the following principles for each transaction:

1. Limit duration when appropriate (to minimise cyclical exposure) and remain opportunistic with repricing.

2. Price loans on either a fixed or floating rate with a floor basis to mitigate against potential reductions in interest rates.

3. Focus on and extensively diligence the loan exit or repayment strategy.

4. Lower our gearing levels and/or introduce higher risk premiums for asset types or geographical areas where markets show signs of illiquidity or

changing fundamentals.

Balancing Short-Term Trade-Offs with Long-Term Returns

In the short term, this approach may mean that we lose out on transactions to competitors who perceive the possibility of lower rates as a risk mitigant, pricing aggressively and offering significant leverage. In contrast, we believe that a measured, dynamic approach grounded in empirical data – rather than expectations – will result in more consistent returns over time. By prioritising resilience and disciplined underwriting, HCP remains well-positioned to weather volatility and capitalise on opportunities sustainably.

At Harbour Credit Partners, we recognise these complexities. Rather than over-relying on rate projections, we adopt a flexible and conservative framework, consistently retesting and updating our assumptions. This approach ensures we remain prepared across varying market environments, focusing on maintaining resilience rather than chasing short-term trends.

About Harbour Credit Partners

Harbour Credit Partners is a Sydney-based private real estate loans manager and a joint venture with the IJD Group, our capital partner. Wholesale investors are eligible to coinvest in loans settled by the HCP investment team and funded via the IJD Group’s balance sheet, with the current available investment opportunities summarised at the following link: https://harbourcreditpartners.portal.agorareal.com/#/public/offerings

Please contact Jonathan Goll, Head of Investor Solutions, with any questions or comments that you might have, or should you need assistance with setting up an account and applying for investment with the firm.

Jonathan Goll

Head of Investor Solutions

M: +61 438 082 247

E: jgoll@harbourcreditpartners.com

Any information or advice contained in this newsletter is general in nature and has been prepared without taking into account your objectives, financial situation or needs. Before acting on any information or advice in this newsletter, you should consider the appropriateness of it (and any relevant product) having regard to your circumstances and, if a current offer document is available, read the offer document before acquiring products named on this website. You should also seek independent financial advice prior to acquiring a financial product.

All financial products involve risks. Past performance of any product described in this newsletter is not a reliable indication of future performance.

Harbour Credit Partners Pty Ltd is the Investment Manager of the Harbour Credit Partners Master Trust. It holds a Corporate Authorised Representative authorisation CAR No.001308393 from Quay Wholesale Fund Services Pty Ltd (Quay) (AFSL No. 528 526). Harbour Credit Partners Pty Ltd also holds a Corporate Authorised Representative authorisation from Quay allowing it to provide General Product Advice.